Robust PCA大法好!

2018-03-01 11:21

141 查看

Robust PCA

When dealing with high-dimensional data sets, we often leverage on the fact that the data has low intrinsic dimensionality in order to alleviate the curse of dimensionality and scale (perhaps it lies in a low-dimensional subspace or lies on a low-dimensional manifold). Principal component analysis is handy for eliminating dimensions.Classical PCA seeks the best rank-kk estimate LL of MM (minimizing ‖M−L‖‖M−L‖ where LL has rank-kk). Truncated SVD makes this calculation!

Traditional PCA can handle small noise, but is brittle with respect to grossly corrupted observations– even one grossly corrupt observation can significantly mess up answer.

Robust PCA factors a matrix into the sum of two matrices, M=L+SM=L+S, where MM is the original matrix, LL is low-rank, and SS is sparse. This is what we’ll be using for the background removal problem!

Low-rank means that the matrix has a lot of redundant information– in this case, it’s the background, which is the same in every scene.

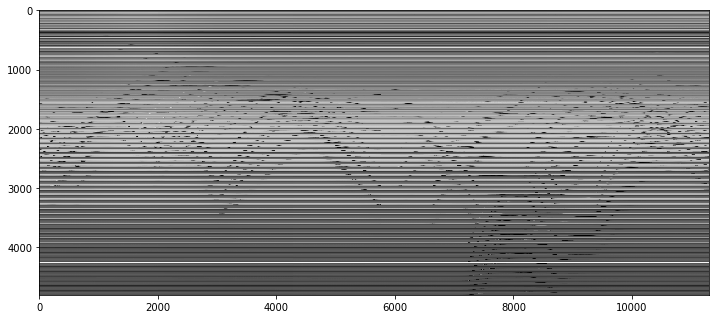

下图是原矩阵 MM (4800, 11300),4800是一帧图片60x80拉长后的向量长度,11300是帧数。图中的solid横线代表background;wave代表行人的moving;column代表 a moment in time。原矩阵 MM 每一列都是某时间点上一帧图像拉长后形成的vector,背景矩阵的rows(图中的horizontal lines)indicates LL 应当是个low-rank的矩阵;

Sparse means that the matrix has mostly zero entries– in this case, see how the picture of the foreground (the people) is mostly empty. (In the case of corrupted data, SS is capturing the corrupted entries. Assume that corrupt data is sparse).

Robust PCA的应用

Face Recognition

下图可以很明显的看到 Low-rank 矩阵就是原图,sparse 矩阵就是人工加上去的噪声!

(Source: Jean Kossaifi)

(Source: Jean Kossaifi)

Robust PCA Optimization

Source

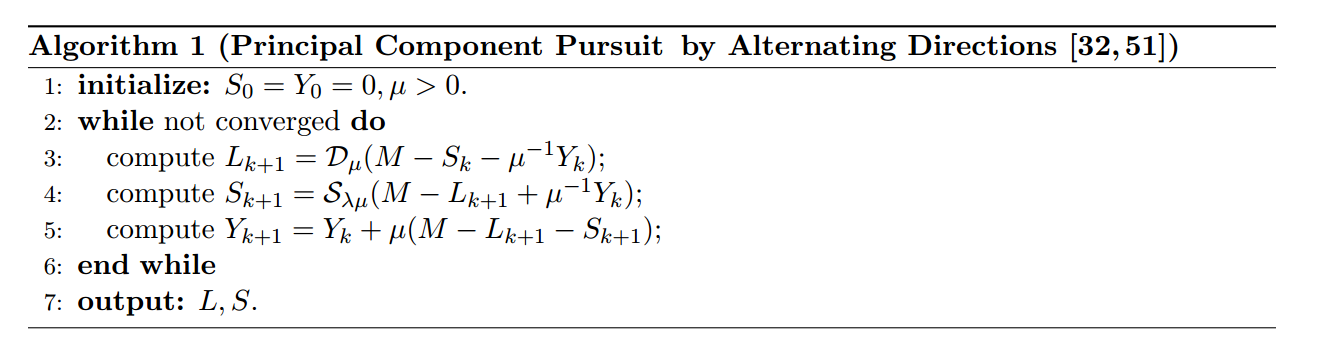

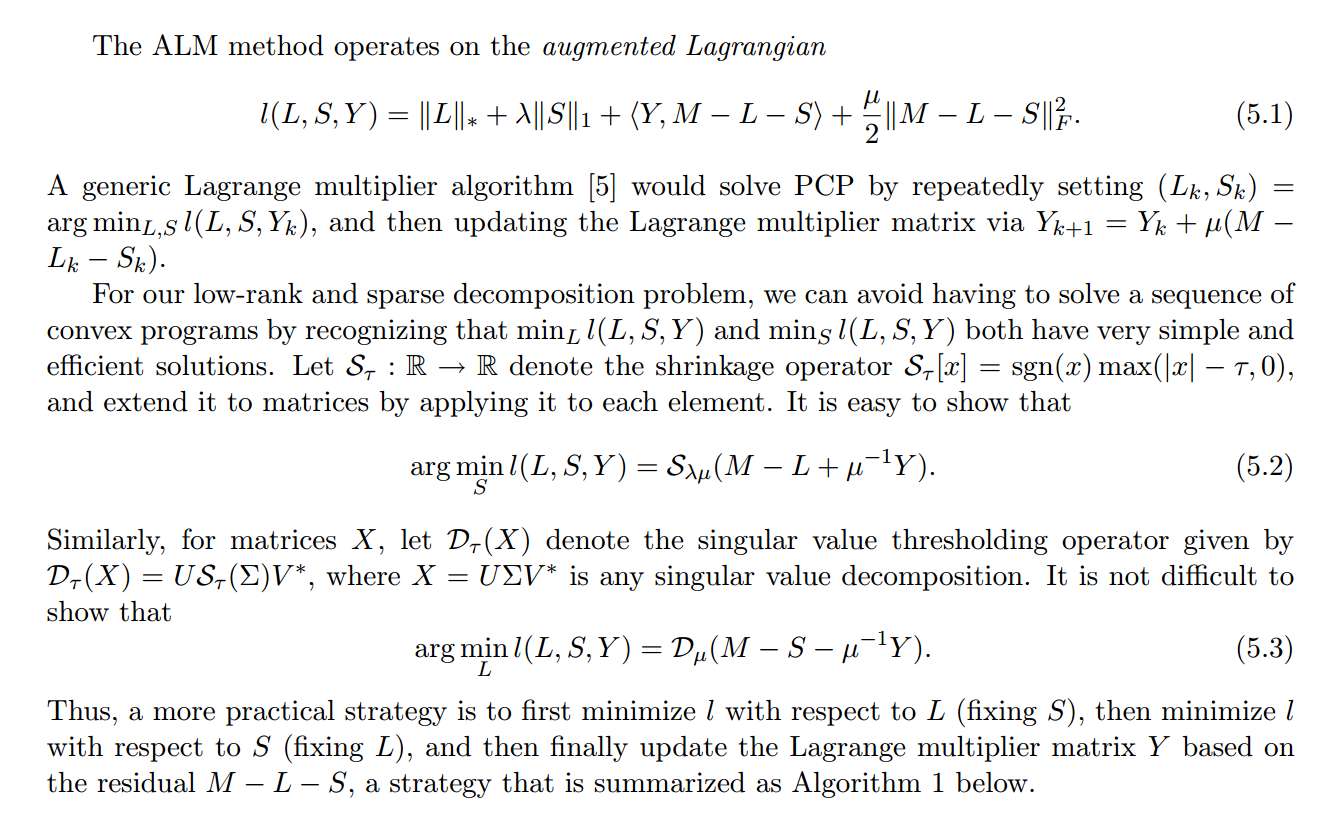

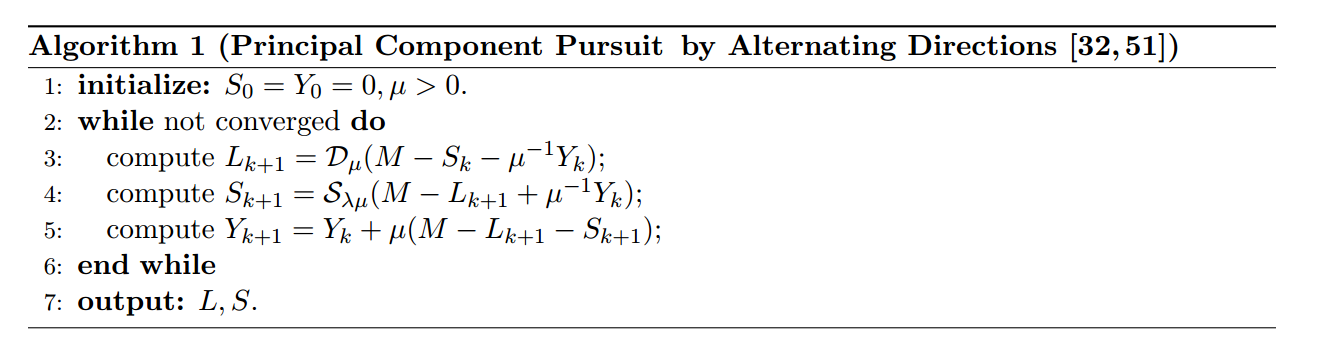

The general primary component pursuit algorithm from this Robust PCA paper (Candes, Li, Ma, Wright), in the specific form of Matrix Completion via the Inexact ALM Method found in section 3.1 of this paper (Lin, Chen, Ma).Optimize Algorithms

I. principal component pursuit

Robust PCA can be written:minimize‖L‖∗+λ‖S‖1subjecttoL+S=Mminimize‖L‖∗+λ‖S‖1subjecttoL+S=M

where:

‖⋅‖1‖⋅‖1 is the L1 norm. Minimizing the L1 norm results in sparse values. For a matrix, the L1 norm is equal to the maximum absolute column norm.

Q:这里为啥用 L1L1 norm呢?

因为 L1L1 norm会lead更好的稀疏性,而我们需要 SS to be a sparse matrix.

‖⋅‖∗‖⋅‖∗ is the nuclear norm, which is the L1 norm of the singular values. Trying to minimize this results in sparse singular values –> low rank.

shrinkage operator Sτ[x]=sgn(x)max(|x|−τ,0)Sτ[x]=sgn(x)max(|x|−τ,0)

取 SS 中的singular value,然后减去 ττ ,如果value比 ττ 小,就round them to 0. 如果 value 大于 ττ 就将两者的差反号,使得singular value更接近0。总的来说这个shrinkage操作就是使得singular value smaller,从而使它们更加sparse。不要忘了我们的目标是:找到一个sparse的 SS。

singular value thresholder DD

就是先对矩阵做SVD分解,然后通过 SS 的 shrinkage 操作使得singular value变小之后,再reconstruct Dτ(X)=USτ(∑)V∗Dτ(X)=USτ(∑)V∗ 得到Low_rank矩阵 LL 的approximation。

这个操作有点像 truncated SVD,也就是说把singular value比较小(小于 ττ)的那些vector cut off。

第3、4步的意思大概是,因为我们的目标是要把原矩阵分解成一个 Low_rank 矩阵 LL 加上一个 Sparse 矩阵 SS ,所以这里我们要不断让 Low_rank矩阵等于原矩阵 MM 减去 Sparse 矩阵 SS,同时让 SS 尽可能等于 M−LM−L。是一个比较典型的交替更新的方法。

而 μ−1Ykμ−1Yk 是为了 keep track of what you still have to approximate(residual error).

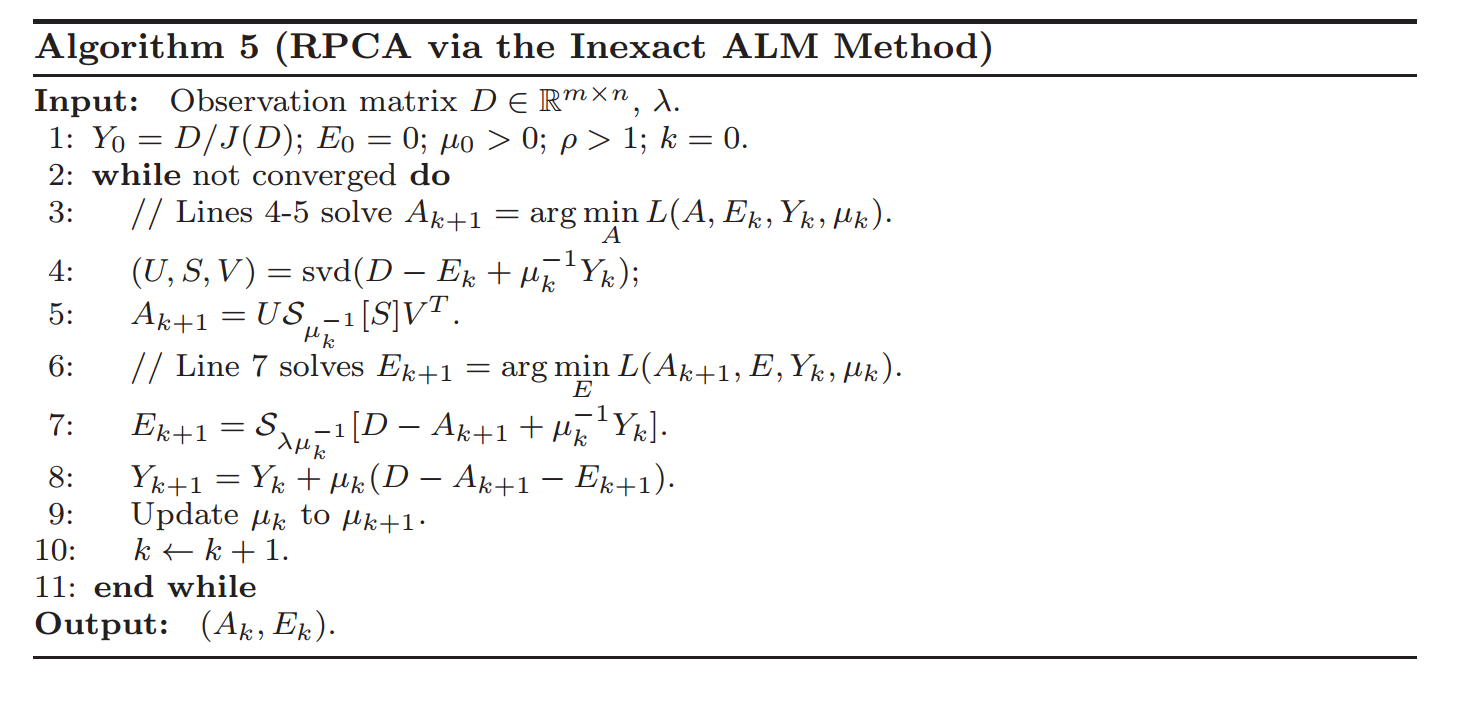

II. ALM

Section 3.1 of Chen, Lin, Ma contains a faster vartiation of this:

And Section 4 has some very helpful implementation details on how many singular values to calculate (as well as how to choose the parameter values):

Implement principal component pursuit

借用 Facebook’s Fast Randomized PCA library实现一发principal component pursuit。from scipy import sparse

from sklearn.utils.extmath import randomized_svd

import fbpca

# TOL是收敛的boundary

TOL=1e-9

MAX_ITERS=3

def converged(Z, d_norm):

err = np.linalg.norm(Z, 'fro') / d_norm

print('error: ', err)

return err < TOLshrinkage operator:把小于 ττ 的singular value都置为0,从另一角度来看就是类似在truncating matrix,ignore那些很小的singular value。

def shrink(M, tau): S = np.abs(M) - tau return np.sign(M) * np.where(S>0, S, 0)

# 写作pca, 读作svd,实际上是一个fast svd implementation def _svd(M, rank): return fbpca.pca(M, k=min(rank, np.min(M.shape)), raw=True) def norm_op(M): return _svd(M, 1)[1][0] # D操作 # 这里的rank是因为fbpca.pca做的是randomized svd,所以需要指定你要保留的rank数 def svd_reconstruct(M, rank, min_sv): u, s, v = _svd(M, rank) # 这里面min_sv就是下面提到的sv s -= min_sv nnz = (s > 0).sum() return u[:,:nnz] @ np.diag(s[:nnz]) @ v[:nnz], nnz

principal component pursuit关键代码实现:

# principal component pursuit是Robust PCA的其中一种algorithm

def pcp(X, maxiter=10, k=10): # refactored

m, n = X.shape

trans = m<n

if trans: X = X.T; m, n = X.shape

lamda = 1/np.sqrt(m)

op_norm = norm_op(X)

Y = np.copy(X) / max(op_norm, np.linalg.norm( X, np.inf) / lamda)

mu = k*1.25/op_norm; mu_bar = mu * 1e7; rho = k * 1.5

d_norm = np.linalg.norm(X, 'fro')

L = np.zeros_like(X); sv = 1

examples = []

for i in range(maxiter):

print("rank sv:", sv)

X2 = X + Y/mu

# update estimate of Sparse Matrix by "shrinking/truncating": original - low-rank

# 对应step 4

S = shrink(X2 - L, lamda/mu)

# update estimate of Low-rank Matrix by doing truncated SVD of rank sv & reconstructing.

# count of singular values > 1/mu is returned as svp

# 对应step 3

L, svp = svd_reconstruct(X2 - S, sv, 1/mu)

'''

这个sv是个划重点的东西,代表了你在truncating svd希望保留的rank数目,这个值需要不停地更新

原始矩阵为400*11300,很明显我们不可能做full svd,肯定贼慢

所以我们先甩掉singular value小于1/μ对应的那些vector,

* 如果我们得到的rank:svp < sv,说明我们想要的value(不小于1/μ的)都已经保留了,

即我们甩掉的value都是该甩的,则下一轮只将 sv + 1(因为第sv之后的singular value也没包含太多信息了)

* 否则即 svp = sv 说明第sv个singular value之后的value可能还有大于1/μ的,

我们甩多了,所以下一轮就要多保留一些sv

看Results中的输出来check一下

'''

# If svp < sv, you are already calculating enough singular values.

# If not, add 20% (in this case 240) to sv

sv = svp + (1 if svp < sv else round(0.05*n))

# residual

Z = X - L - S

Y += mu*Z; mu *= rho

# keep track Time=140 时的visual

examples.extend([S[140,:], L[140,:]])

if m > mu_bar: m = mu_bar

if converged(Z, d_norm): break

if trans: L=L.T; S=S.T

return L, S, examplesResults

m, n = M.shape round(m * .05) #240

L, S, examples = pcp(M, maxiter=5, k=10)

rank sv: 1 error: 0.131637937114 rank sv: 241 error: 0.0458515689041 rank sv: 49 error: 0.00588796042886 rank sv: 289 error: 0.000565564416732 rank sv: 529 error: 2.47254909523e-05

sv 初始化为 1,然后加上 n 的 20%,即 240。

然后 svp = 48 < 241,所以 sv = 48 + 1 =49。

相关文章推荐

- Robust PCA 学习笔记

- Robust PCA 学习笔记

- 最优化之Robust PCA

- 拉格朗日乘子解Robust PCA以及Python实现

- PCA大法好!

- 笔记:Online Robust PCA via Stochastic Optimization

- Robust PCA——Inexect ALM

- 视频前背景分离论文之(1) Online Robust PCA via Stochastic Optimization

- Robust PCA (摘抄)

- Robust PCA 学习笔记

- Robust PCA 学习笔记

- PCA 与 Robust PCA区别

- [转]Robust PCA 学习笔记

- Robust PCA

- 视频前背景分离论文之(5) Robust PCA via Nonconvex Rank Approximation

- Robust PCA Low-rank(附matalb 代码)

- Building a Robust Web Based Email Client (WebMail) Using the IP*Works! ADO.NET Data Provider(原文)

- Robust Estimation for Range Image Segmentation and Reconstruction

- 欢乐园网吧免费上网大法

- robust object detection