风险平价组合- Risk Parity: A Bullet-Proof Investment Strategy?

2017-01-17 22:04

936 查看

本文转载自:http://seekingalpha.com/article/868521-risk-parity-a-bullet-proof-investment-strategy?page=2#

The basic idea behind risk parity is to diversify a portfolio in terms of risk, but not in terms of dollar values. In other words, risk is spread equally between asset classes so that each asset class contributes the same amount

of volatility to the portfolio rather than an equal amount of capital. A traditional balanced portfolio, where 60 percent is allocated in equities and the remaining 40 percent is invested in bonds, may look balanced from a capital allocation point of view,

instead of from a risk perspective.

In our article, we would like to compare a traditional 60/40 portfolio with a risk parity approach, which uses the same underlying asset classes. In our comparison, we will use the SPDR S&P 500 ETF (NYSEARCA:SPY)

to represent the allocation to equities and the iShares Barclays 20+ Year Treasury Bond (NYSEARCA:TLT)

as well as the iShares iBoxx $ Invest Grade Corp Bond (NYSEARCA:LQD) to represent the fixed income investments.

In our example, there is no allowance for transaction costs or brokerage fees.

By applying a risk parity approach, it is absolute necessary to determine the weightings of each asset class on a regular basis, since the correlation among asset classes is not stable over time. For that reason, we are using a

rolling covariance matrix to determine the appropriate weights for each asset class to ensure that each asset class contributes the same amount of risk.

Moreover, we have calculated the risk contribution of each asset class for a traditional balanced portfolio, where 60 percent is invested in the SPDR S&P 500 ETF , 20 percent being put into the iShares Barclays 20+ Year Treasury

Bond and the remaining 20 percent are allocated to the iShares iBoxx $ Invest Grade Corp Bond .

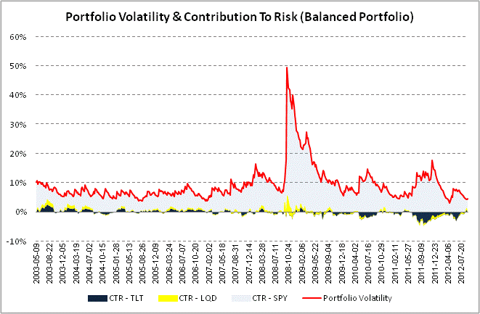

By adding up each contribution to risk, we will receive the overall portfolio volatility at a specific point of time. The volatility of the balanced portfolio is mainly driven by the 60 percent investment in equities while bonds

just contribute very little risk (Chart 1). Especially in times of market turbulence, like in 2008, the diversification benefits are reduced significantly as equities are the main risk contributor within the portfolio. If an asset class is negative correlated

to the remaining ones at a specific point of time, then its contribution to risk turns negative (for example TLT during 2011). Therefore, investors could easily put more weight to that specific asset class, without having to increase the total portfolio volatility.

This effect can be also seen as the diversification potential of that specific asset class. That is exactly where the risk parity portfolio comes into play.

Chart 1: Volatility and CTR - Balanced Portfolio

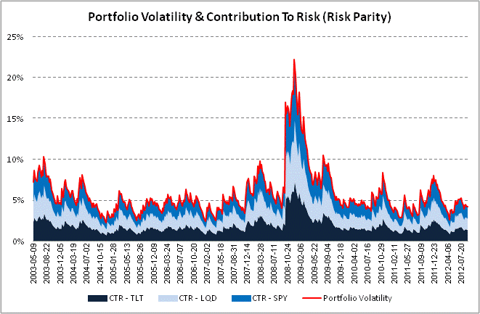

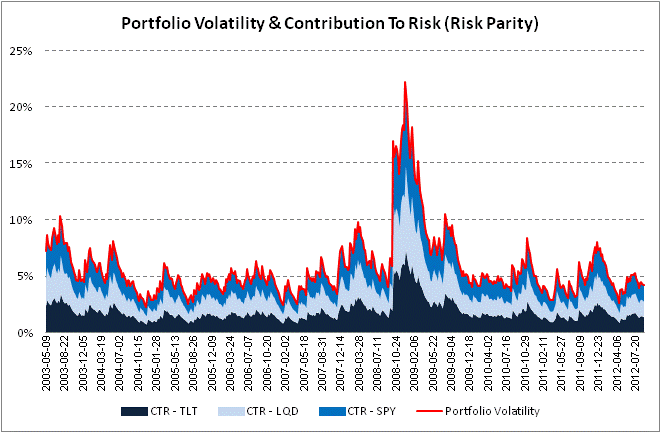

As each asset class contributes the same amount of risk, its diversification potential is much better utilized compared with a traditional balanced portfolio. If we have a closer look at the risk parity portfolio

(Chart 2), we can see that each asset class contributes the same amount of risk at any given time, although the portfolio volatility changes over time. For that reason, the average volatility of the risk parity portfolio is much lower compared

with the traditional investment strategy. Many institutional investors (e.g. Bridgewater) are using leverage to keep the portfolio volatility at a certain target level and to increase the overall portfolio performance).

Chart 2: Volatility and CTR - Risk Parity Portfolio

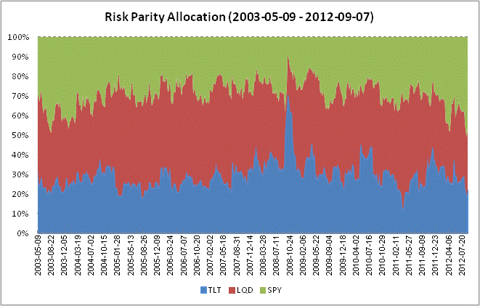

If we have a look at the specific weightings within the risk parity portfolio, we can see that on average, 30 percent is invested in the SPDR S&P 500 ETF , 41 percent is invested in the iShares iBoxx $ Invest Grade Corp Bond and

the remaining 29 percent are allocated to the iShares Barclays 20+ Year Treasury Bond (Chart 3).

Chart 3: Historical Allocation - Risk Parity

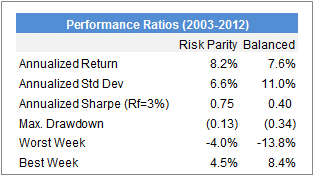

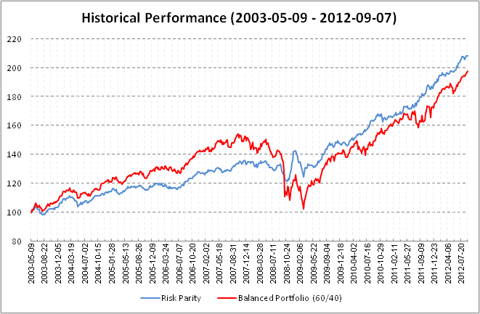

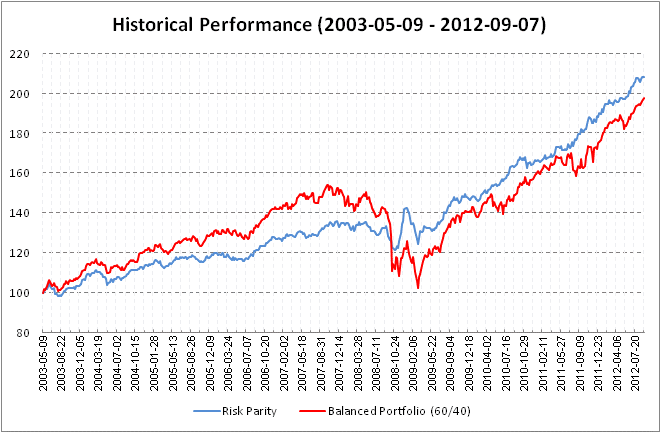

Since we have only focused on the contribution to risk so far, we would like to examine how these two portfolios have been performing the past. Table 1 presents the results of our back tests from Sept. 5, 2003 until Sept. 7, 2012 on the two portfolios

described previously (including one day slippage). The first column tests the risk parity approach while the second on represents a traditional balanced portfolio.

Table 1: Performance and Risk Ratios

Chart 4: Payoff

The risk parity has an annualized return of 8.16% while a buy and hold has only generated an annualized rate of return of 7.55%. More importantly, on a risk-adjusted basis (Sharpe Ratio), the equal risk portfolio is strongly outperforming the traditional weighting.

Nevertheless, the risk parity portfolio is underperforming the traditional one, when the stock market is in a strong bull market without any major market turns (like in 2003 until 2007).

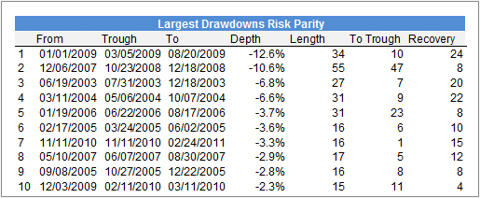

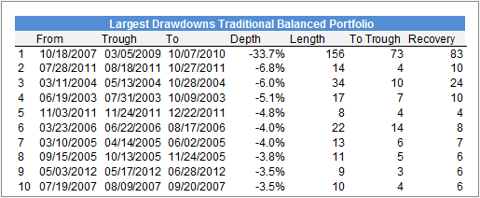

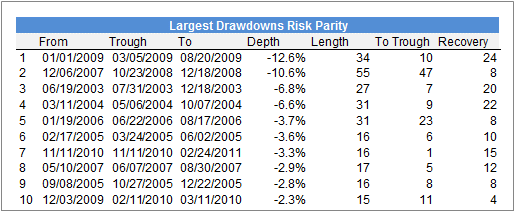

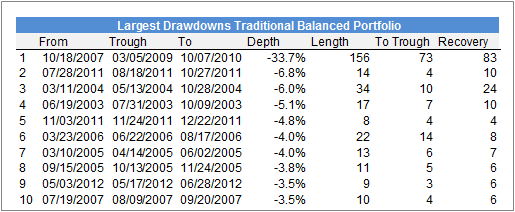

If we have a closer look on the diversification benefits (reducing risk during turbulent market conditions), we can see that the risk parity has also shown significant lower draw-downs in the past. The maximum draw down for the risk parity portfolio was only

12.6 percent, compared with 33.7 percent for the balanced approach. That makes roughly 2 times more. In total, the risk parity portfolio was reaching a new high after 34 weeks compared with 156 weeks for the balanced

portfolio.

The bottom line: risk parity is a good alternative approach if investors are searching for a highly diversified portfolio. Since it can fully utilize the benefits of diversification, so then the portfolio is able to reduce draw-downs considerably,

especially in times of market turbulence. Nevertheless, the outcome of the strategy depends mainly by chosen asset classes, as this investment strategy allocates the most to those ETFs which have the lowest volatility. Therefore please

bear in mind, that any approach is only as good as the expected future value of its underlying asset classes as well as their diversification characteristics.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no

business relationship with any company whose stock is mentioned in this article.

The basic idea behind risk parity is to diversify a portfolio in terms of risk, but not in terms of dollar values. In other words, risk is spread equally between asset classes so that each asset class contributes the same amount

of volatility to the portfolio rather than an equal amount of capital. A traditional balanced portfolio, where 60 percent is allocated in equities and the remaining 40 percent is invested in bonds, may look balanced from a capital allocation point of view,

instead of from a risk perspective.

In our article, we would like to compare a traditional 60/40 portfolio with a risk parity approach, which uses the same underlying asset classes. In our comparison, we will use the SPDR S&P 500 ETF (NYSEARCA:SPY)

to represent the allocation to equities and the iShares Barclays 20+ Year Treasury Bond (NYSEARCA:TLT)

as well as the iShares iBoxx $ Invest Grade Corp Bond (NYSEARCA:LQD) to represent the fixed income investments.

In our example, there is no allowance for transaction costs or brokerage fees.

By applying a risk parity approach, it is absolute necessary to determine the weightings of each asset class on a regular basis, since the correlation among asset classes is not stable over time. For that reason, we are using a

rolling covariance matrix to determine the appropriate weights for each asset class to ensure that each asset class contributes the same amount of risk.

Moreover, we have calculated the risk contribution of each asset class for a traditional balanced portfolio, where 60 percent is invested in the SPDR S&P 500 ETF , 20 percent being put into the iShares Barclays 20+ Year Treasury

Bond and the remaining 20 percent are allocated to the iShares iBoxx $ Invest Grade Corp Bond .

By adding up each contribution to risk, we will receive the overall portfolio volatility at a specific point of time. The volatility of the balanced portfolio is mainly driven by the 60 percent investment in equities while bonds

just contribute very little risk (Chart 1). Especially in times of market turbulence, like in 2008, the diversification benefits are reduced significantly as equities are the main risk contributor within the portfolio. If an asset class is negative correlated

to the remaining ones at a specific point of time, then its contribution to risk turns negative (for example TLT during 2011). Therefore, investors could easily put more weight to that specific asset class, without having to increase the total portfolio volatility.

This effect can be also seen as the diversification potential of that specific asset class. That is exactly where the risk parity portfolio comes into play.

Chart 1: Volatility and CTR - Balanced Portfolio

As each asset class contributes the same amount of risk, its diversification potential is much better utilized compared with a traditional balanced portfolio. If we have a closer look at the risk parity portfolio

(Chart 2), we can see that each asset class contributes the same amount of risk at any given time, although the portfolio volatility changes over time. For that reason, the average volatility of the risk parity portfolio is much lower compared

with the traditional investment strategy. Many institutional investors (e.g. Bridgewater) are using leverage to keep the portfolio volatility at a certain target level and to increase the overall portfolio performance).

Chart 2: Volatility and CTR - Risk Parity Portfolio

If we have a look at the specific weightings within the risk parity portfolio, we can see that on average, 30 percent is invested in the SPDR S&P 500 ETF , 41 percent is invested in the iShares iBoxx $ Invest Grade Corp Bond and

the remaining 29 percent are allocated to the iShares Barclays 20+ Year Treasury Bond (Chart 3).

Chart 3: Historical Allocation - Risk Parity

Since we have only focused on the contribution to risk so far, we would like to examine how these two portfolios have been performing the past. Table 1 presents the results of our back tests from Sept. 5, 2003 until Sept. 7, 2012 on the two portfolios

described previously (including one day slippage). The first column tests the risk parity approach while the second on represents a traditional balanced portfolio.

Table 1: Performance and Risk Ratios

Chart 4: Payoff

The risk parity has an annualized return of 8.16% while a buy and hold has only generated an annualized rate of return of 7.55%. More importantly, on a risk-adjusted basis (Sharpe Ratio), the equal risk portfolio is strongly outperforming the traditional weighting.

Nevertheless, the risk parity portfolio is underperforming the traditional one, when the stock market is in a strong bull market without any major market turns (like in 2003 until 2007).

If we have a closer look on the diversification benefits (reducing risk during turbulent market conditions), we can see that the risk parity has also shown significant lower draw-downs in the past. The maximum draw down for the risk parity portfolio was only

12.6 percent, compared with 33.7 percent for the balanced approach. That makes roughly 2 times more. In total, the risk parity portfolio was reaching a new high after 34 weeks compared with 156 weeks for the balanced

portfolio.

The bottom line: risk parity is a good alternative approach if investors are searching for a highly diversified portfolio. Since it can fully utilize the benefits of diversification, so then the portfolio is able to reduce draw-downs considerably,

especially in times of market turbulence. Nevertheless, the outcome of the strategy depends mainly by chosen asset classes, as this investment strategy allocates the most to those ETFs which have the lowest volatility. Therefore please

bear in mind, that any approach is only as good as the expected future value of its underlying asset classes as well as their diversification characteristics.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no

business relationship with any company whose stock is mentioned in this article.

相关文章推荐

- Bullet(Cocos2dx)之凸多面体形状和组合形状

- 债券投资组合信用风险与利率风险对冲策略

- RQPro 公募FOF策略实例——晨星基金筛选和风险平价配置

- 风险种类是有关你和你的投资组合

- 基于风险平价的资产配置策略

- 51CTO之任意密码存在重置风险(各种组合综合利用) 20160328

- 【codechef】Strategy for the World Cup(组合打表)

- 组合索引怎么应该怎么选取引导列?

- [oracle] rownum、order by 组合实现top N

- 给定一个正整数数组,找所有元素组合起来最大的值(答案)

- 【组合数学】POJ_1850_Code

- Luogu 2822(组合数学)(NOIP2016)

- 组合问题(递归)

- 探索组合索引的数据存储

- Eclipse中10个最有用的快捷键组合

- bzoj 2142 礼物 (组合数学+数论)

- 项目简单实用方式_组合替代继承_算法切换

- .Net 绑定Dropdownlist的时自定义组合字段后显示

- URAL 1994 The Emperor's plan 求组合数 大数用log+exp处理

- 自定义组合控件关于LayoutInflater.from(context).inflate(R.layout.view_title, this,true)的问题